What Is a Home Appraisal? Complete Guide for Homeowners (2026)

If you're buying a home or refinancing your mortgage, you'll almost certainly encounter the home appraisal. For many first-time buyers, this required step can seem mysterious or even stressful. Understanding what happens during an appraisal, why lenders require them, and what to expect can help demystify this critical part of the real estate transaction.

After working with thousands of appraisals across diverse markets, we've seen how this process protects both buyers and lenders while ensuring fair market transactions. This guide walks you through everything you need to know about home appraisals in 2026.

What Is a Home Appraisal?

A home appraisal is an independent, professional assessment of a property's market value. A licensed or certified appraiser conducts this evaluation, examining the physical characteristics of the home and comparing it to recent sales of similar properties in the area. The result is a detailed report that provides an objective opinion of what the property is worth in the current market.

Unlike a home inspection, which focuses on the condition and potential problems with a property, an appraisal focuses specifically on determining fair market value. The appraiser isn't working for the buyer or seller. Their job is to provide an unbiased valuation based on market data and professional analysis.

Why Lenders Require Appraisals

Lenders don't require appraisals to frustrate homebuyers. They need this independent valuation to manage risk and make sound lending decisions.

When a bank loans you money to purchase a home, that property serves as collateral for the loan. If you're unable to make payments and the lender must foreclose, they need confidence that they can recover their investment by selling the property. An appraisal helps establish what the home is actually worth, separate from what a motivated buyer might be willing to pay in a competitive situation.

The appraisal also establishes the loan-to-value ratio, or LTV. This percentage compares the loan amount to the appraised value. For example, if you're buying a home appraised at $400,000 with a $320,000 loan, your LTV is 80%. Generally, lower LTV ratios represent less risk for lenders and may qualify borrowers for better interest rates or terms.

In most purchase transactions, federal regulations require lenders to obtain an appraisal for loans secured by real estate. This isn't just internal policy. It's a regulatory requirement designed to promote safe and sound lending practices.

Types of Home Appraisals

Not all appraisals involve an appraiser walking through your home with a clipboard. In 2026, several different appraisal types exist, each appropriate for different situations.

Full Interior Appraisal

This is the traditional appraisal most people envision. The appraiser visits the property, conducts a complete interior and exterior inspection, measures the home, photographs key features, and notes the condition and quality of construction. They'll observe the layout, count bedrooms and bathrooms, check the kitchen and bath updates, and assess overall condition. This comprehensive approach provides the most detailed valuation and is typically required for purchase transactions and most refinances.

Desktop Appraisal

A desktop appraisal relies on existing data, public records, previous appraisals, and sometimes photos provided by the homeowner or agent. The appraiser doesn't visit the property but instead analyzes comparable sales and available property information from their office. These appraisals can be completed more quickly and at lower cost, making them suitable for certain refinance scenarios or when recent appraisal data already exists.

Exterior-Only Appraisal

Sometimes called a drive-by appraisal, this approach involves the appraiser visiting the property to observe and photograph the exterior and neighborhood but not entering the home. They rely on public records, MLS data, and other sources for interior details. This option balances cost and speed with some level of direct property observation.

The type of appraisal your lender requires depends on the loan type, transaction purpose, property characteristics, and current lending guidelines. In recent years, more flexibility has emerged in appraisal types, particularly for refinances and properties with recent prior appraisals.

What Appraisers Look for During Inspection

During a full interior appraisal, the appraiser is gathering information that will help them determine market value. While they're noting condition issues, they're not inspecting systems the way a home inspector would.

Appraisers typically examine:

- Overall size and layout of the home, including gross living area

- Number of bedrooms, bathrooms, and other rooms

- Quality of construction and materials used

- Age and condition of major systems (HVAC, electrical, plumbing)

- Kitchen and bathroom updates and condition

- Flooring, walls, and ceiling condition

- Garage, basement, or attic spaces

- Lot size, landscaping, and exterior condition

- Any additional features like pools, decks, or outbuildings

- Overall appeal compared to other homes in the market

The appraiser is also observing the neighborhood, nearby properties, and location factors that influence value. Proximity to schools, shopping, employment centers, and major roads all factor into market value.

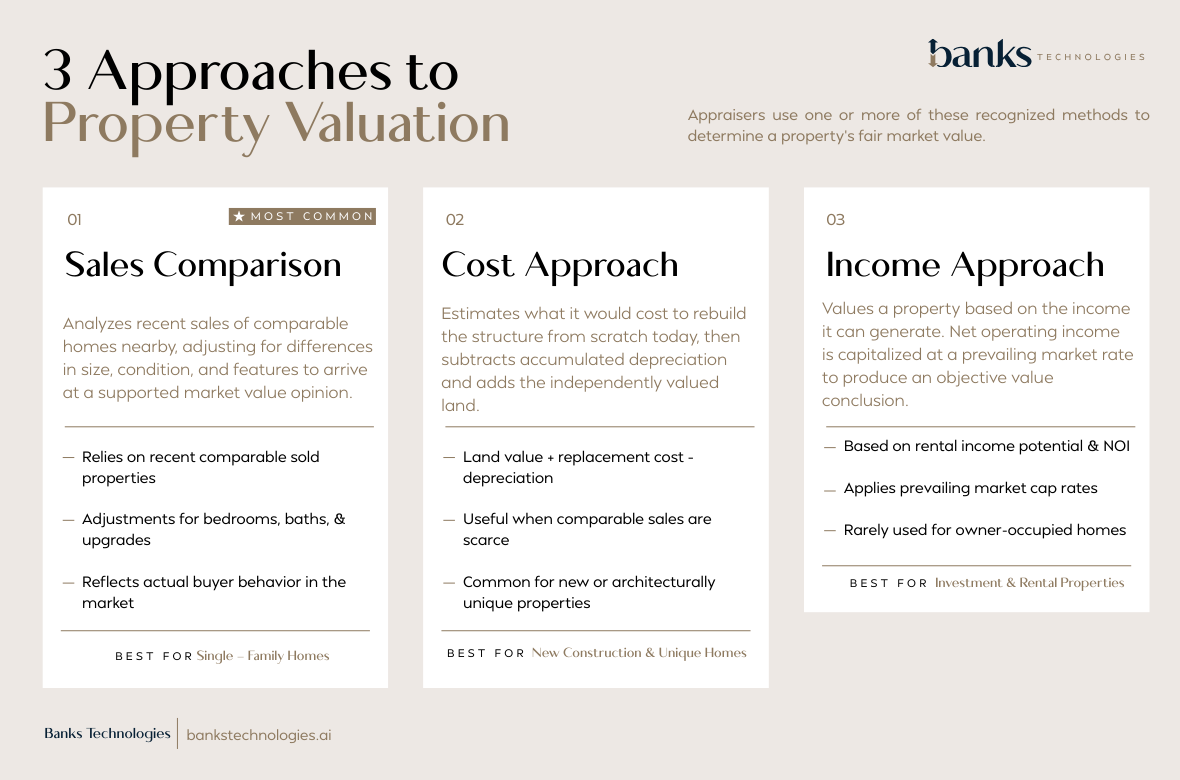

How Appraisers Determine Value

Appraisers use three recognized approaches to value, though not all apply to every property type.

Sales Comparison Approach

This is the primary method for single-family homes. The appraiser identifies recently sold properties similar to the subject property in terms of location, size, age, condition, and features. These comparable sales, or comps, provide market evidence of what buyers are actually paying for similar homes.

The appraiser then makes adjustments to account for differences between the comps and the subject property. If a comparable home has an extra bathroom, the appraiser adjusts its sale price downward to make it more comparable to the subject. If the subject property has a finished basement that a comp lacks, an upward adjustment to the comp reflects that difference.

These adjustments are based on market data showing how specific features impact value in that particular market. What matters is what buyers in that specific market will pay for various features and differences.

Cost Approach

This approach estimates what it would cost to rebuild the home from scratch, accounting for depreciation and adding the land value. While less commonly the primary approach for existing homes, it can be useful for newer construction or unique properties without good comparable sales.

Income Approach

This approach is primarily used for investment properties and estimates value based on the income the property could generate. For typical owner-occupied single-family homes, this approach usually isn't applicable.

For most residential appraisals, the sales comparison approach carries the most weight in the final value conclusion, as it most directly reflects what the market is actually doing.

Timeline: How Long Does an Appraisal Take?

Once your lender orders the appraisal, the timeline typically breaks down as follows:

- Appraiser assignment and scheduling: 1-3 days

- Property inspection: 30-60 minutes on site

- Research, analysis, and report completion: 3-7 days

- Total turnaround time: 5-10 days in most markets

These timelines can vary based on market conditions, property complexity, and appraiser workload. In busy markets or rural areas with fewer appraisers, turnaround times may extend. Complex or high-value properties requiring more extensive research may also take longer.

Technology platforms have helped improve turnaround times in recent years by streamlining order management, communication, and report delivery, though the fundamental research and analysis work still requires professional expertise and time.

Cost: What to Expect to Pay

Appraisal costs vary based on location, property type, and complexity. In 2026, typical ranges include:

- Standard single-family home: $400-$600

- Larger or more complex properties: $600-$1,000+

- Desktop or exterior-only appraisals: $150-$300

- Multi-family or unique properties: $800-$2,000+

In purchase transactions, buyers typically pay for the appraisal, though this can sometimes be negotiated. For refinances, the homeowner pays this cost, which is usually collected upfront or rolled into closing costs.

While it might be tempting to view the appraisal as just another fee, remember that this independent assessment protects you from overpaying for a property and ensures you're not borrowing more than the property can reasonably support.

What Happens If the Appraisal Comes In Low

A low appraisal, where the appraised value comes in below the agreed purchase price, can create challenges but doesn't necessarily kill the transaction. Several options exist:

Renegotiate the Purchase Price

The buyer can ask the seller to lower the price to match the appraised value. In some markets, sellers may agree, particularly if they're motivated or if the appraisal reveals legitimate concerns about their pricing.

Increase the Down Payment

If the buyer has additional funds available, they can bring more cash to closing to cover the gap between the appraised value and purchase price. This maintains the agreed purchase price while keeping the lender's LTV ratio within acceptable limits.

Challenge the Appraisal

If there are legitimate concerns about the appraisal, such as inappropriate comparable sales or factual errors about the property, the buyer or their agent can provide additional information for the appraiser's consideration. Appraisers may reconsider their value conclusion if presented with compelling market data they didn't initially consider.

Walk Away

Most purchase contracts include an appraisal contingency that allows buyers to cancel the contract if the appraisal comes in low. While disappointing, this protects buyers from overpaying.

A low appraisal isn't necessarily bad news. It may be protecting you from paying more than market value for a property, which could create problems when you eventually sell or refinance.

How Technology Is Improving the Appraisal Process

The appraisal industry has evolved significantly in recent years. Better data sources, improved communication platforms, and streamlined workflows have made the process more efficient for everyone involved.

Homeowners now often receive better communication about scheduling and timing. Digital platforms enable faster report delivery and clearer presentation of valuation data. While the core professional judgment required for accurate appraisals hasn't changed, the tools supporting that work have improved substantially.

This evolution benefits homeowners through faster turnarounds, more consistent service, and improved transparency into how valuations are determined. The human expertise at the center of the appraisal process remains essential, but better technology makes that expertise more accessible and efficient.

Key Takeaways

- A home appraisal is an independent professional assessment of a property's market value, required by lenders to manage risk and ensure sound lending decisions

- Different appraisal types exist, including full interior, desktop, and exterior-only approaches, each appropriate for different situations

- Appraisers primarily use the sales comparison approach for residential properties, analyzing recent comparable sales and making adjustments for differences

- Typical appraisals cost $400-$600 for standard homes and take 5-10 days from order to report delivery

- A low appraisal isn't necessarily bad news—it may protect you from overpaying and can often be addressed through renegotiation, additional down payment, or providing additional market data

- The appraisal protects all parties in the transaction by providing an objective assessment of value separate from what a motivated buyer might offer in a competitive situation

Understanding the appraisal process helps you navigate real estate transactions with confidence, knowing what to expect and why this step matters for your financial protection.